Your Parent's Medicare Bill Just Hit $200. Here's What Gets Cut First.

The number arrived quietly, the way most bad news does when you're old and on a fixed income. In November 2025, the Centers for Medicare and Medicaid Services announced that the standard Part B premium for 2026 would be $202.90 per month. It was the first time the premium had ever crossed $200.

For policy analysts, this was a data point. For the 67 million people enrolled in Medicare, it was a grocery decision.

The Real Numbers

Let's lay them out, because the specifics matter more than the headlines.

Monthly costs:

- Medicare Part B premium: $202.90 (up $17.90 from 2025)

- Higher-income beneficiaries pay more through IRMAA surcharges

Annual deductibles:

- Part B deductible: $283 (up $26)

- Part A hospital deductible: $1,736 per benefit period (up $60)

- Part D prescription drug deductible: up to $615 (up $25)

If your parent needs skilled nursing:

- Days 1 through 20: $0 copay after hospital deductible

- Days 21 through 100: $217 per day in coinsurance

- Day 101 onward: your parent pays everything

That skilled nursing line is where you get blindsided. A 30-day skilled nursing stay after a hip fracture costs $2,170 out of pocket just in coinsurance. A 60-day stay: $8,680. And after day 100? The meter runs at full rate. Every dollar.

Where the Money Goes

Social Security's 2026 cost-of-living adjustment gave retirees a modest bump. For the average beneficiary, that increase was roughly $50 per month. The Medicare premium increase alone eats more than a third of it.

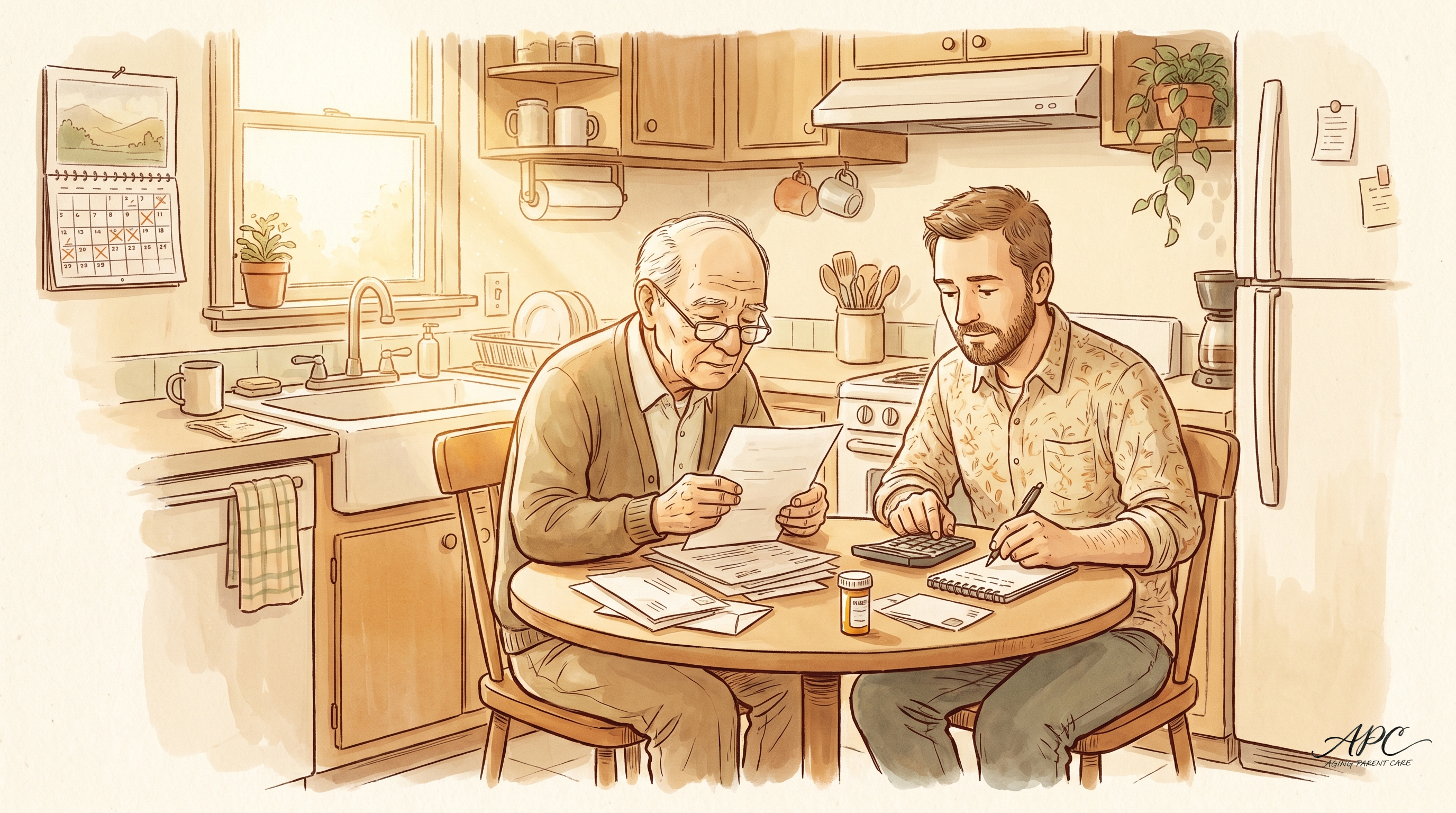

Here's what that looks like on a kitchen table in Dayton, Ohio, where retired postal worker Gerald Tran sits down with his daughter Michelle every month to go through his bills:

Gerald's Social Security check: $1,927 per month.

After Medicare Part B: $1,724.

After his Medigap supplement: $1,564.

After Part D prescription plan: $1,519.

After his two blood pressure medications and one statin (copays): $1,471.

That leaves $1,471 for rent, utilities, food and transportation. Gerald's one-bedroom apartment in Dayton costs $875. After rent, he's got $596 for the month. For everything.

Gerald isn't poor enough for Medicaid. He isn't rich enough to absorb a $1,736 hospital deductible without panic. He occupies the vast middle where most American retirees live: one bad fall from financial crisis.

What Medicare Doesn't Cover (and You Won't Expect)

Here's the thing: the most common misconception about Medicare is that it covers long-term care. It doesn't.

Medicare doesn't pay for:

- Assisted living (median cost: $6,313 per month in 2026)

- Custodial care (help with bathing, dressing, eating)

- Most home health aide services beyond short-term skilled needs

- Adult day programs

- Long-term nursing home stays

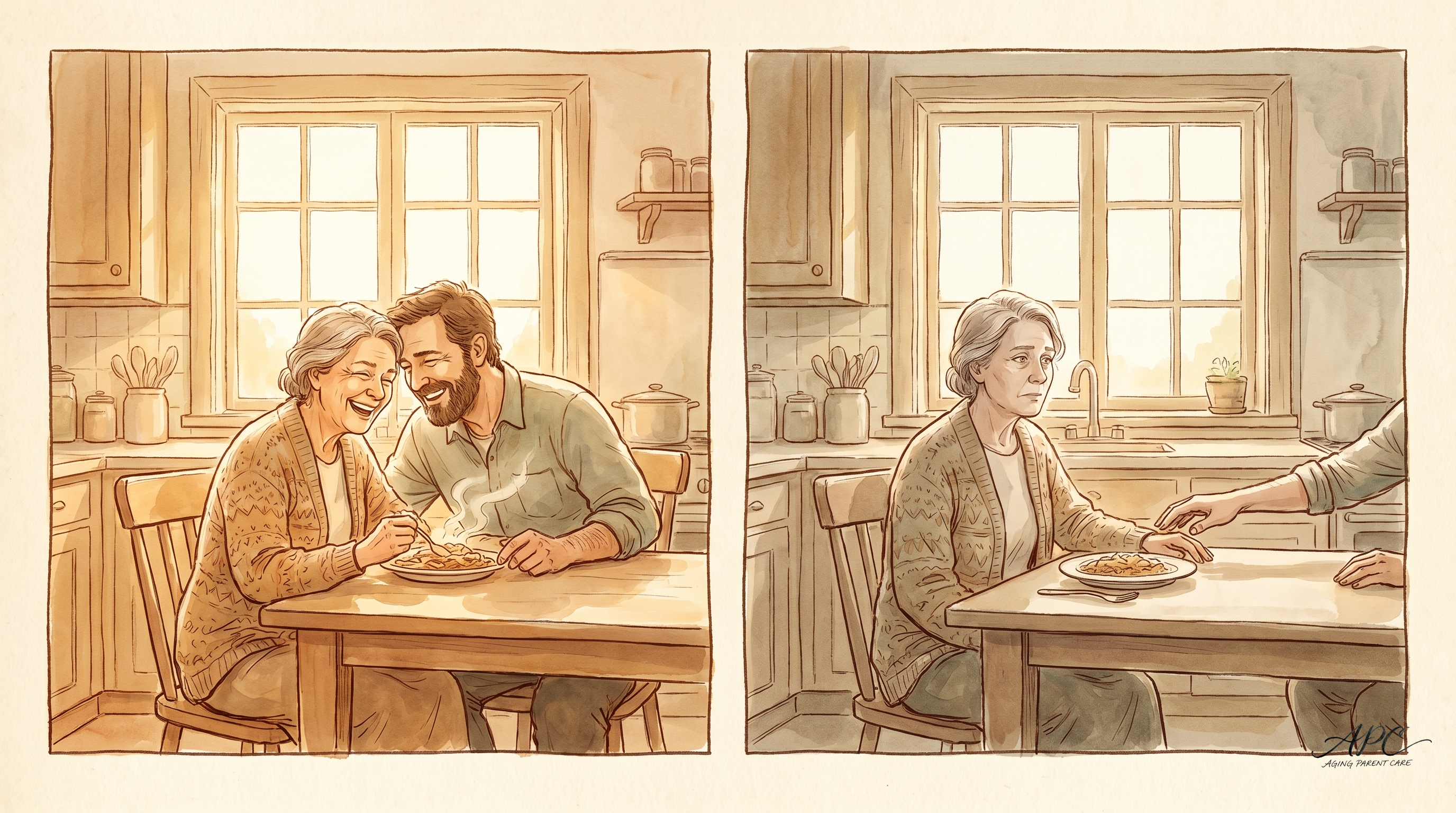

You discover this at the worst possible moment: when your parent has just been discharged from the hospital and needs daily help. The social worker says "Medicare doesn't cover this," and you're staring at your siblings across a hospital room trying to figure out who's paying $6,000 a month.

The Medicaid Cliff

Medicaid does cover long-term care, but qualifying requires near-total impoverishment. In most states, a single applicant must have less than $2,000 in countable assets. Some states have expanded this, but the core reality stays the same: your parent has to spend down nearly everything they own before Medicaid steps in.

This creates a brutal calculation. Do you spend your parent's savings on care now, knowing that once the money runs out, Medicaid will cover a nursing home but not the assisted living facility where they've made friends? Do you pay privately for as long as possible, knowing that every month of private pay is a month of inheritance evaporating? Sound familiar?

These aren't theoretical questions. They happen at kitchen tables every day, in cities like Dayton and Duluth, wherever a family has a parent and a savings account and a gap between the two.

Three Things to Do This Month

If your parent is on Medicare and you haven't reviewed their costs recently, here's where to start.

Check for Extra Help. Medicare's Extra Help program (also called the Low-Income Subsidy) can cut Part D costs significantly. And the eligibility thresholds are higher than most people think: in 2026, individuals with income under roughly $22,000 and assets under $17,000 may qualify. You can apply through Social Security at ssa.gov/medicare/part-d-extra-help or by calling 1-800-772-1213.

Review the Medigap plan. If your parent has a Medicare Supplement policy, compare it to current alternatives during the open enrollment period. Plans F and G are the most common, but premiums vary wildly by insurer. A 30-minute call to SHIP (State Health Insurance Assistance Program, 877-839-2675), a free counseling service, can identify savings. Michelle Tran in Dayton used SHIP last October and found a Plan G option that saved Gerald $47 a month with identical coverage. Thirty minutes, $47 a month. Worth it.

Talk about the five-year lookback. Medicaid examines five years of financial transactions when someone applies. Gifts or transfers within that window can trigger penalties. If there's any chance your parent will need Medicaid-funded long-term care, an elder law attorney consultation now (typical cost: $250 to $500) could save tens of thousands later.

The Conversation Nobody Wants to Have

Most of us don't know our parents' financial situation in any detail. It feels intrusive to ask. It feels premature. It feels like you're treating your parent like a problem to be solved.

But the $202.90 premium is a useful door opener. It's concrete. It's happening to everyone on Medicare. It's not personal.

You might say: "I saw Medicare premiums went up again. How's that landing for you? Do you want to sit down and look at the numbers together?"

That's it. Not a demand. Not an intervention. Just an opening.

Because the worst version of this story is the one where Gerald Tran's daughter Michelle finds out about the hospital deductible after the fall, finds out about the skilled nursing copay after the discharge, finds out about the Medicaid spend-down requirement after the savings are gone.

The numbers aren't going to get smaller. So when do you start that conversation?

Sources

- CMS. CMS Releases 2026 Medicare Parts B and D Premiums. November 2025.

- Medicare.gov. Medicare Part A Costs.

- KFF. An Overview of the Medicare Part D Prescription Drug Benefit. 2025.

- Genworth Financial. Cost of Care Survey 2025.

- Medicaid.gov. Medicaid Eligibility.

- SSA. Extra Help with Medicare Prescription Drug Plan Costs. 2026.

© 2026 Aging Parent Care. All rights reserved. No portion of this article may be reproduced, distributed, or used in any form without the explicit written permission of Aging Parent Care.

Make Your Business Online By The Best No—Code & No—Plugin Solution In The Market.

30 Day Money-Back Guarantee

Say goodbye to your low online sales rate!